Custom likelihoods: Tweedie regression on insurance claims

A latent Gaussian model in Latte is not tied to a fixed list of observation likelihoods. Any distribution you can write down as a logpdf can go on the ~ line of an @latte model and be fit with inla(), recovering posterior marginals for the latent field and the hyperparameters together.

This tutorial works through that on the Tweedie compound Poisson-Gamma, the standard model for zero-inflated continuous responses such as insurance claim amounts, daily rainfall, and fish-catch biomass, where most observations are exactly zero and the rest are continuous and right-skewed.

We will:

wrap a hand-coded log-density as a

Distributionsubtype usable in an@lattemodel,let Latte's adapter route the custom

~statement through its automatic-differentiation observation model without touching theinla()call, andrecover the regression coefficients and the dispersion hyperparameter from a single fit.

Why Tweedie?

A Tweedie distribution with power parameter 1 < p < 2 is a compound Poisson-Gamma, the member of the Tweedie exponential-dispersion family that handles zero-inflated continuous data: each observation Y arises by first drawing a count N ~ Poisson(λ) and then summing N iid Gamma claim sizes,

When N = 0 the sum is zero (no claim). When N ≥ 1 the sum is a continuous, right-skewed Gamma-shaped quantity. The parameters fold into a clean (mean, dispersion, power) parametrisation,

with λ = μ^(2-p)/(φ(2-p)), α = (2-p)/(p-1), β = φ(p-1)μ^(p-1). The power variance function, with variance scaling like μ^p, gives Tweedie its range: p = 1 is Poisson, p = 2 is Gamma, and 1 < p < 2 interpolates between them.

A custom Distribution

The Tweedie pdf has no closed form, but Dunn & Smyth (2005) give a numerically stable series expansion that is a few lines of Julia.

We use the compound Poisson-Gamma form. At y = 0 the density is atomic, P(Y = 0) = exp(-λ). For y > 0 it factors as

and we sum the inner series in log-space with the standard log-sum-exp trick.

using Distributions

using Distributions: loggamma

"Compute log Σ_{n=1}^{n_max} term(n) with log-sum-exp stabilisation."

function _tweedie_log_W(y, μ, φ, p; n_max::Int = 150)

α = (2 - p) / (p - 1)

log_y = log(y)

log_λ = (2 - p) * log(μ) - log(φ * (2 - p))

log_β = log(φ * (p - 1)) + (p - 1) * log(μ)

log_term(n) = n * log_λ - loggamma(n + 1) +

n * α * (log_y - log_β) - loggamma(n * α)

m = log_term(1)

@inbounds for n in 2:n_max

t = log_term(n)

if t > m

m = t

end

end

s = zero(m)

@inbounds for n in 1:n_max

s += exp(log_term(n) - m)

end

return m + log(s)

end

"Tweedie compound Poisson-Gamma log-density at `y` with mean μ, dispersion φ, power p ∈ (1,2)."

function tweedie_logpdf(y, μ, φ, p)

log_λ = (2 - p) * log(μ) - log(φ * (2 - p))

if y == 0

return -exp(log_λ)

else

log_β = log(φ * (p - 1)) + (p - 1) * log(μ)

return -exp(log_λ) - y / exp(log_β) - log(y) +

_tweedie_log_W(y, μ, φ, p)

end

endMain.var"##996".tweedie_logpdfTo use this inside an @latte model, we wrap it as a small Distribution subtype with a logpdf, which is all Latte needs to recognise the ~ statement and route it through its automatic-differentiation observation model. The three parameters get independent type parameters so that the latent-derived μ (an AD dual number) and φ/p (a hyperparameter and a constant) can carry different types. That is what keeps the struct AD-ready, and it avoids the need for a promoting constructor.

struct Tweedie{A, B, C} <: ContinuousUnivariateDistribution

μ::A

φ::B

p::C

end

Distributions.logpdf(d::Tweedie, y::Real) = tweedie_logpdf(y, d.μ, d.φ, d.p)A quick sanity check: as p → 2 the compound Poisson-Gamma collapses to a single Gamma. The limiting parameters come from the compound representation: with N ~ Poisson(λ) Poisson-many Gamma(α, β) claims, Y has approximate Gamma shape λ·α = μ^(2-p)/(φ(p-1)) and scale β = φ(p-1)μ^(p-1). As p → 2, λ·α → 1/φ and β → φμ. So at any p close to 2 our tweedie_logpdf should approach Gamma(λ·α, β) — and at p ≈ 2 exactly, Gamma(1/φ, φμ).

let μ = 5.0, φ = 1.0, p = 1.99, y = 4.0

λα = μ^(2 - p) / (φ * (p - 1)) # limiting Gamma shape

β = φ * (p - 1) * μ^(p - 1) # limiting Gamma scale

(tweedie_logpdf(y, μ, φ, p), logpdf(Gamma(λα, β), y))

end(-2.4025734870815825, -2.3949828400519615)Match within ~0.01 nats — the residual closes as p → 2.

Simulating an insurance-style dataset

We simulate n = 200 policies. Each policy has a single covariate (a standardised driver-risk score). The mean claim is log-linear: log μ = β₀ + β₁ · x. Truth: β = [2.0, -0.4], φ = 1.5, p = 1.6.

using LinearAlgebra

using Random

using DataFrames

function rand_tweedie(rng, μ, φ, p)

λ = μ^(2 - p) / (φ * (2 - p))

α = (2 - p) / (p - 1)

β_scale = φ * (p - 1) * μ^(p - 1)

n = rand(rng, Poisson(λ))

n == 0 && return 0.0

return rand(rng, Gamma(n * α, β_scale))

end

Random.seed!(42)

n = 200

true_β = [2.0, -0.4]

X = hcat(ones(n), randn(n))

true_μ = exp.(X * true_β)

true_φ = 1.5

true_p = 1.6

y = [rand_tweedie(Random.GLOBAL_RNG, μ_i, true_φ, true_p) for μ_i in true_μ]

df = DataFrame(x = X[:, 2], claim = y, has_claim = y .> 0)

first(df, 5)5×3 DataFrame

Row │ x claim has_claim

│ Float64 Float64 Bool

─────┼────────────────────────────────

1 │ -0.363357 16.2249 true

2 │ 0.251737 4.57096 true

3 │ -0.314988 6.68916 true

4 │ -0.311252 3.5185 true

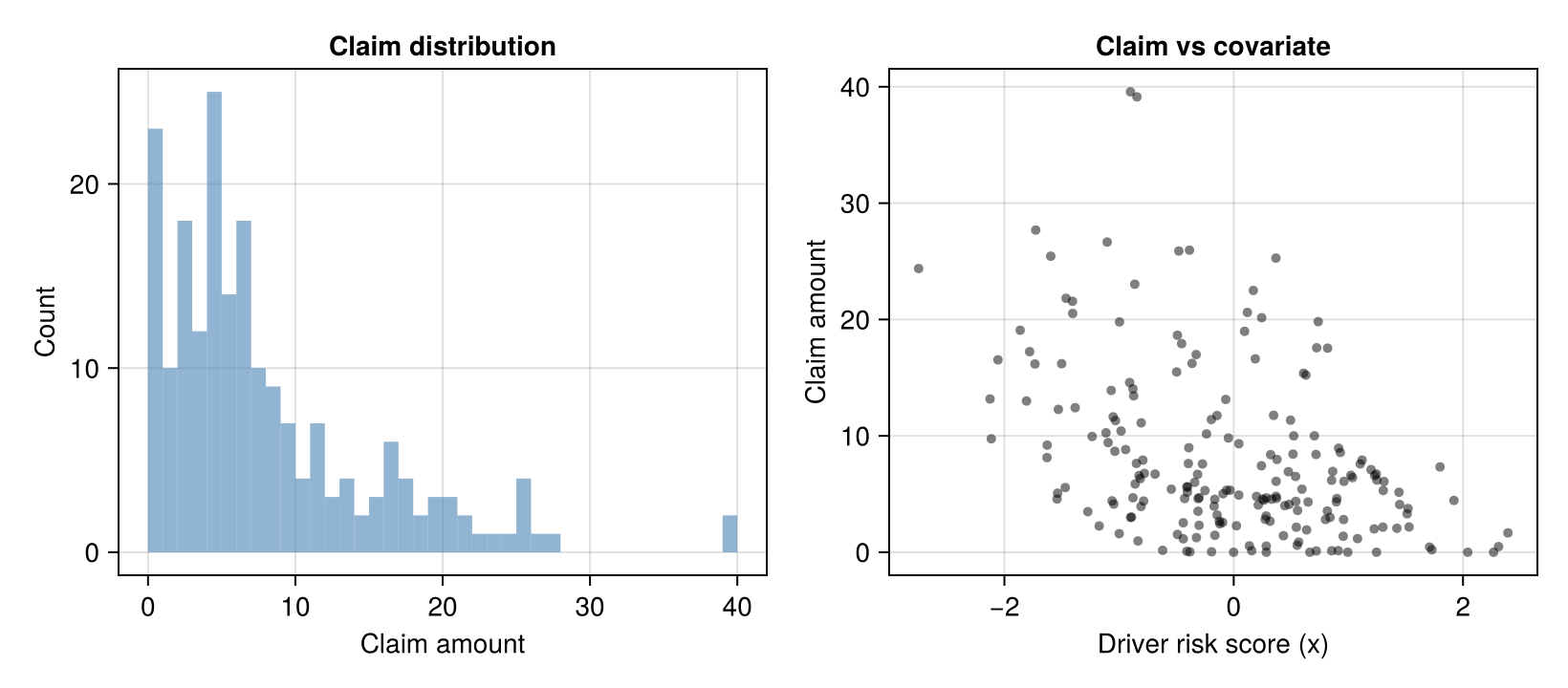

5 │ 0.816307 3.54193 trueAbout 4% of policies file no claim at all; the rest are continuous, right-skewed claim amounts. The claim distribution and its dependence on the covariate are two different views of the same df, so we build each as an AlgebraOfGraphics layer and draw them into one figure:

using AlgebraOfGraphics, CairoMakie

fig = Figure(size = (820, 360))

draw!(

fig[1, 1],

data(df) * mapping(:claim => "Claim amount") *

AlgebraOfGraphics.histogram(bins = 40) *

visual(color = (:steelblue, 0.6));

axis = (title = "Claim distribution", ylabel = "Count"),

)

draw!(

fig[1, 2],

data(df) * mapping(:x => "Driver risk score (x)", :claim => "Claim amount") *

visual(Scatter, markersize = 7, color = (:black, 0.5));

axis = (title = "Claim vs covariate",),

)

fig

The cluster of zero-claim policies plus the long right tail is the zero-inflated-continuous shape Tweedie was designed for.

The model

The @latte model has the same shape as any other Latte regression: a hyperparameter prior, a Gaussian prior on the regression coefficients, and a ~ statement per observation. The only custom piece is the Tweedie(...) distribution.

We treat the Tweedie power p as a fixed domain choice (p = 1.6 is typical for claim severity). That keeps the hyperparameter dimension at one and focuses the inference on the dispersion φ and the regression coefficients β. To learn p from the data instead, you would add it as another ~ line and Latte would integrate over it as well.

using Latte

@latte function tweedie_glm(y, X, p_fixed)

φ ~ LogNormal(0.0, 2.0)

β ~ MvNormal(zeros(size(X, 2)), 100.0 * I(size(X, 2)))

for i in eachindex(y)

μ_i = exp(dot(X[i, :], β))

y[i] ~ Tweedie(μ_i, φ, p_fixed)

end

endtweedie_glm (generic function with 1 method)A few notes on what happens under the hood:

The custom Tweedie likelihood is not in Latte's fast-path table (Poisson, Bernoulli, Binomial, Normal, NegativeBinomial, Gamma), so the adapter routes it through

AutoDiffObservationModel. That covers anylogpdfwe can write, including ones with an infinite series like Tweedie, at the cost of a little more compile time on the first call.We pass

likelihood_hessian_pattern = :densebecause the Tweedie series expansion is not traceable bySparseConnectivityTracer; theforloop over series terms breaks tracer propagation. Forn = 200a dense Hessian is small, and for very largenyou would supply a known sparse pattern explicitly.Calling the

@lattefunction returns theLatentGaussianModel. Latte readsφas a hyperparameter andβas the latent field. Because the priorLogNormal(0, 2)has positive support, the log-transform is inferred automatically and theφmarginal is reported in natural (dispersion) space.

lgm = tweedie_glm(y, X, true_p; likelihood_hessian_pattern = :dense)LatentGaussianModel

├─ hyperparameters (1)

│ φ ~ LogNormal(μ=0.0, σ=2.0) [log]

├─ latent field · 2 dims

│ β 2

└─ likelihood

custom logpdf · 200 observationsRunning INLA

Declaring the prior directly on the natural parameter φ means there is no hyperparameter-derived value for @latte to hoist into the observation payload, so this model runs under the default diff_strategy = ADStrategy() with no extra wiring; the AD path handles a hand-written logpdf without trouble. We pass FiniteDiffStrategy() here as a performance choice: for a custom likelihood with a single hyperparameter, finite differences are about twice as fast as AD on the outer Hessian, and nothing else about the call changes.

result = inla(

lgm, y;

diff_strategy = FiniteDiffStrategy(),

progress = false,

)INLAResult:

Model: LatentGaussianModel{HyperparameterSpec{@NamedTuple{φ::Hyperparameter{Base.Fix1{typeof(broadcast), typeof(log)}, :natural}}, @NamedTuple{}}, Latte._PatternAugmentedLatentModel{Latte.RoutedLatentModel{FixedEffectsModel{LinearSolve.DiagonalFactorization, Nothing}, @NamedTuple{}}, SparseArrays.SparseMatrixCSC{Bool, Int64}}, Latte._LiftedSingleObsModel{GaussianMarkovRandomFields.AutoDiffObservationModel{typeof(Main.var"##996".__latte_obs_body_tweedie_glm), ADTypes.AutoForwardDiff{nothing, Nothing}, ADTypes.AutoSparse{ADTypes.AutoForwardDiff{nothing, Nothing}, ADTypes.KnownHessianSparsityDetector{SparseArrays.SparseMatrixCSC{Bool, Int64}}, SparseMatrixColorings.GreedyColoringAlgorithm{:direct, 1, Tuple{SparseMatrixColorings.NaturalOrder}}}, Tuple{Symbol}, typeof(Main.var"##996".__latte_obs_pointwise_tweedie_glm)}, typeof(Main.var"##996".__latte_prelude_tweedie_glm), @NamedTuple{y::Vector{Float64}, X::Matrix{Float64}, p_fixed::Float64}, Tuple{Symbol}, @NamedTuple{β::UnitRange{Int64}}, @NamedTuple{β::Bool}, Tuple{Symbol}}}

Hyperparameters: 1

Latent variables: 2

Mode: (φ=1.5258)

Convergence: ✓

Total time: 25.60 seconds

Exploration: 5 points (5 integration)

Model comparison metrics:

Deviance Information Criterion (DIC):

DIC: 1214.58

Effective parameters (p_D): 0.93

Mean deviance (D̄): 1213.66

Deviance at mode: 1212.73

Marginal Log-Likelihood:

log p(y): -619.85

Watanabe-Akaike Information Criterion (WAIC):

WAIC: 1218.44

Effective parameters (p_WAIC): 2.69

Log pointwise predictive density (lppd): -606.53

Conditional Predictive Ordinates (CPO):

LPML: -602.8

Mean CPO: 0.063

Min CPO: 0.0009

Approximation quality (KLD):

Max SKLD: 0.0000 (variable 1)

Mean SKLD: 0.0000

Use .hyperparameter_marginals, .latent_marginals, .accumulators for analysisPosteriors

latent_marginals(result, :β) returns the posterior marginals for the regression coefficients, and hyperparameter_marginals(result, :φ) returns the marginal for φ in natural (dispersion) space, since we declared the prior on φ directly. Each is a Distributions.jl-compatible object, so mean, std, quantile, and the rest work on them directly. summary_df collects the common statistics into a table:

β_summary = summary_df(latent_marginals(result, :β))2×6 DataFrame

Row │ mode median q2_5 q97_5 mean std

│ Float64 Float64 Float64 Float64 Float64 Float64

─────┼────────────────────────────────────────────────────────────────

1 │ 1.9853 1.9853 1.86871 2.10189 1.9853 0.0594443

2 │ -0.40657 -0.406571 -0.525494 -0.287642 -0.40657 0.0606363...and the dispersion marginal:

hp_summary = summary_df(hyperparameter_marginals(result, :φ))1×6 DataFrame

Row │ mode median q2_5 q97_5 mean std

│ Float64 Float64 Float64 Float64 Float64 Float64

─────┼───────────────────────────────────────────────────────

1 │ 1.51307 1.5271 1.32807 1.75723 1.53154 0.111988Compare to truth:

truth = DataFrame(

parameter = ["β₁ (intercept)", "β₂ (slope)", "φ"],

truth = [true_β[1], true_β[2], true_φ],

posterior_mean = [β_summary.mean[1], β_summary.mean[2], hp_summary.mean[1]],

q2_5 = [β_summary.q2_5[1], β_summary.q2_5[2], hp_summary.q2_5[1]],

q97_5 = [β_summary.q97_5[1], β_summary.q97_5[2], hp_summary.q97_5[1]],

)3×5 DataFrame

Row │ parameter truth posterior_mean q2_5 q97_5

│ String Float64 Float64 Float64 Float64

─────┼───────────────────────────────────────────────────────────────

1 │ β₁ (intercept) 2.0 1.9853 1.86871 2.10189

2 │ β₂ (slope) -0.4 -0.40657 -0.525494 -0.287642

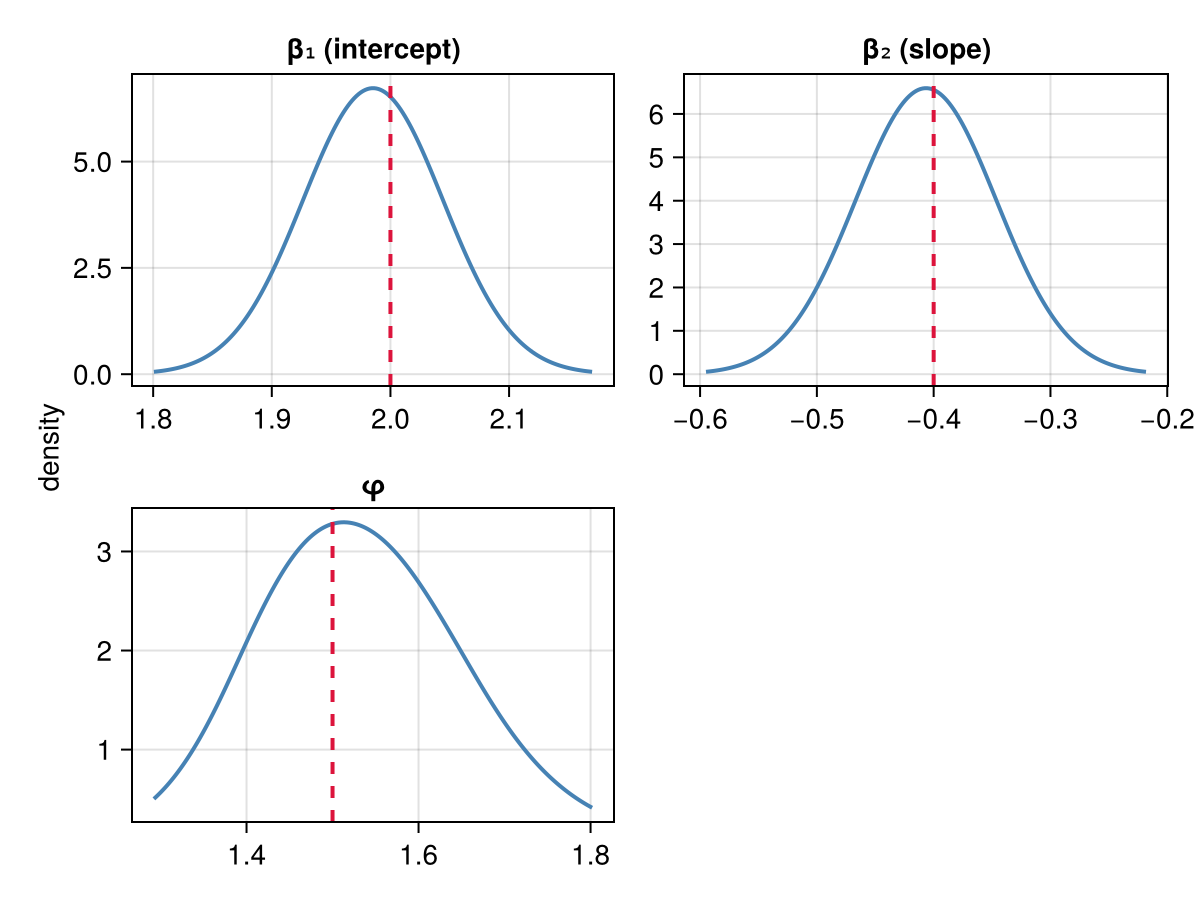

3 │ φ 1.5 1.53154 1.32807 1.75723All three true values land inside the 95% credible intervals. We can also plot the marginal posteriors. Each panel covers a different variable on its own scale, so we assemble a tidy density table from the accessors and facet it, with the true values as a second layer of reference lines:

β_marginals = latent_marginals(result, :β)

φ_marginal = hyperparameter_marginals(result, :φ)[1]

panels = [

("β₁ (intercept)", β_marginals[1], true_β[1]),

("β₂ (slope)", β_marginals[2], true_β[2]),

("φ", φ_marginal, true_φ),

]

density_df = mapreduce(vcat, panels) do (name, marginal, _)

xs = range(quantile(marginal, 0.001), quantile(marginal, 0.999); length = 200)

DataFrame(parameter = name, value = xs, density = pdf.(marginal, xs))

end

truth_df = DataFrame(

parameter = [name for (name, _, _) in panels],

truth = [true_val for (_, _, true_val) in panels],

)

curves = data(density_df) *

mapping(:value, :density, layout = :parameter) *

visual(Lines, color = :steelblue, linewidth = 2)

truth_lines = data(truth_df) *

mapping(:truth, layout = :parameter) *

visual(VLines, color = :crimson, linestyle = :dash, linewidth = 2)

draw(curves + truth_lines; facet = (; linkxaxes = :none, linkyaxes = :none))

Red dashed lines mark the true values; the posteriors concentrate around them. The dispersion posterior centres on φ ≈ 1.5, the generative truth.

Takeaway

A distribution you can express as logpdf(::MyDist, y) works as an observation likelihood in Latte without any change to the inla() call. The same model shape would carry an ordinal likelihood, a heavy-tailed Student-t, or a Bayesian quantile regression built on the asymmetric Laplace. This fit ran under the default ADStrategy(); we used FiniteDiffStrategy() only as a speed optimisation for the single-hyperparameter outer Hessian.

A few practical tips when writing your own:

Keep the

logpdfAD-friendly. Control flow should branch ony(data, fixed) rather than on the parameters, and avoidFloat64-typed buffers in the body; use comprehensions orsimilar(x, T)so the eltype propagates from the inputs.If the

logpdfinvolves an iterative computation (a series, root solver, or ODE solver) that sparsity tracing cannot see through, passlikelihood_hessian_pattern = :denseon the@lattemodel to skip pattern detection.When the likelihood is conditionally independent, which covers most cases, supplying

pointwise_loglik_funclets Latte use a faster diagonal-Hessian path. The adapter wires this up automatically; if you build theLatentGaussianModelby hand, pass it toAutoDiffObservationModelyourself.ADStrategy()handles the outer hyperparameter gradient for custom likelihoods by default.FiniteDiffStrategy()is a reasonable alternative with only a handful of hyperparameters, where finite differences are cheap and ran somewhat faster here.

For other applications of this pattern, see the rest of the tutorials: hierarchical regressions, smoothing priors, and spatial models.

References

The numerically stable series expansion of the Tweedie density used here: a log-sum-exp evaluation of the compound Poisson-Gamma infinite series.

The exponential-dispersion family that contains the Tweedie distributions, including the compound Poisson-Gamma with power variance function Var[Y] = φ μ^p.

This page was generated using Literate.jl.